Every bank in the world has a cybersecurity team. Most have firewalls, intrusion detection systems, dedicated SOCs, and multi-million dollar security budgets. By 2024, the average cost of a data breach in the financial sector reached $6.08 million — 22% higher than the global cross-industry average. And yet, most banks leave their single most critical digital asset — their domain name — in the hands of a third-party registrar that can be compromised, pressured, or coerced without the bank's knowledge.

That is the gap Handshake TLDs close.

The Problem Nobody Talks About: DNS Is Not Secure

When a customer types mybank.com into their browser, they trust that what comes back is genuinely their bank. That trust is almost entirely unfounded.

The Domain Name System was designed in 1983 for resilience, not security. At every step of the resolution chain — from the recursive resolver to the authoritative nameserver — data can be intercepted, spoofed, or modified. The root zone is controlled by ICANN, a US-based organisation still subject to US law. And the TLD itself is leased, not owned: a registrar issues you access to a name, and that same registrar can suspend, redirect, or hand over that name under legal or operational pressure.

A rogue DNS server can translate domain names of financial institutions into IP addresses of malicious sites — and forged security certificates can be used to perform man-in-the-middle attacks that decrypt banking traffic and re-encrypt it before forwarding to the original destination, leaving both parties unaware that credentials or transaction details have been captured.

This is not a theoretical scenario. In 2019, the Sea Turtle DNS hijacking campaign targeted banks and financial institutions across the Middle East. Attackers re-registered nameservers at the registrar level, intercepted login pages, and harvested credentials — all while valid SSL certificates continued to display green padlocks. The bank's own servers were never touched. The attack happened entirely at the DNS layer, in infrastructure the bank didn't control.

Financial institutions in 2026 are being attacked through the systems and relationships that make modern finance work: digital identity, remote access, cloud infrastructure, customer devices, and third-party providers. DNS is one of those third-party dependencies — and it is the one most banks have done the least to address.

What a Handshake TLD Changes

Handshake is a decentralised, permissionless blockchain whose sole purpose is the ownership of DNS root-zone names. Unlike ICANN — where a TLD is a leasehold issued and controlled by a registrar — Handshake encodes TLD ownership as a UTXO on a proof-of-work blockchain. The holder of a Handshake TLD holds a cryptographic private key. No registrar, no government, and no court order can revoke, redirect, or suspend that domain without possessing that key.

The security guarantee is mathematically precise: the probability of an adversary forging TLD ownership without the private key is 1/2²⁵⁶ — the same security level as Bitcoin. This is not a policy guarantee or a service-level agreement. It is a cryptographic property of the system itself.

For a bank, this means something concrete: a financial institution that operates under a Handshake TLD — for example .bankname — owns its internet identity absolutely. Every second-level domain beneath it (accounts.bankname, api.bankname, kyc.bankname) is issued by the bank itself, not by any third-party registrar. No external entity can issue a subdomain under the bank's TLD. No external entity can suspend it. The namespace is sovereign.

The Six Attack Vectors Legacy DNS Cannot Defend Against

Here is a direct comparison of what ICANN DNS and Handshake TLDs offer against the most common banking-level DNS threats:

1. DNS Hijacking — An attacker steals registrar credentials and modifies the bank's DNS records, redirecting customers to a phishing clone. Under ICANN DNS, the bank's domain security is only as strong as its registrar's login page. Under Handshake, modifying DNS records requires the bank's blockchain private key — stored in a hardware security module (HSM) that never goes online.

2. Registrar Seizure — A court order forces the registrar to suspend the domain. The bank goes offline instantly, regardless of its own operational status. Under Handshake, there is no registrar to serve a court order to. The blockchain has no compliance mechanism; the TLD is a UTXO, not a database record.

3. Rogue Certificate Authority — Forged SSL certificates can impersonate financial institutions, allowing attackers to decrypt encrypted banking traffic. ICANN-based domains trust over 200 certificate authorities globally — any one of them can issue a valid-looking certificate for any domain. Handshake eliminates this by supporting DANE (DNS-Based Authentication of Named Entities), which pins the exact TLS certificate in a TLSA record on the blockchain. Even if a rogue CA issues a certificate for accounts.bankname, the TLSA mismatch causes browser rejection before a single byte of customer data is transmitted.

4. BGP Hijacking — Route advertisement spoofing at the ISP level intercepts traffic before it reaches the bank's servers. While Handshake doesn't directly prevent BGP attacks, DANE certificate pinning ensures that even if traffic is redirected, the TLS handshake fails immediately — making the interception useless.

5. Typosquatting — Under ICANN, anyone can register myb4nk.com or my-bank.com and build a convincing phishing site. Under Handshake, only the TLD owner can issue second-level domains. Nobody can register accounts.bankname or any variation of it without the bank's explicit issuance. The namespace is closed by design.

6. Government Censorship — In jurisdictions where banking services may be politically targeted, a government can instruct a registrar or DNS provider to block or redirect a domain. Handshake resolution is decentralised: there is no single point of control to apply pressure to.

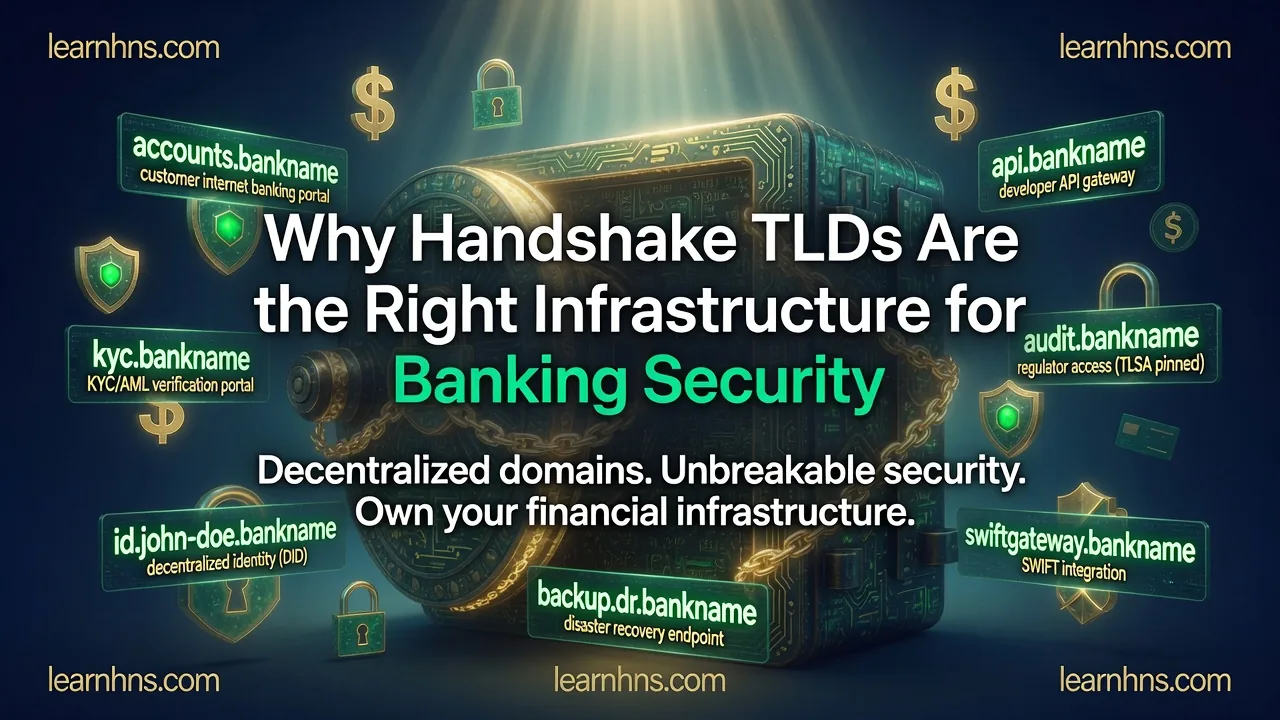

How It Works in Practice: The .bankname Example

Consider a bank that acquires the Handshake TLD .bankname. The bank's CTO holds the private key in an HSM. Here is how the namespace looks:

accounts.bankname— the customer internet banking portalapi.bankname— the developer API gateway for FinTech integrationskyc.bankname— the KYC/AML verification portalaudit.bankname— regulator access, with cryptographic certificates pinned via TLSAid.john-doe.bankname— per-customer decentralised identity (DID) documentswift-gateway.bankname— SWIFT messaging integrationbackup.dr.bankname— disaster recovery endpoint

Every one of these addresses is issued by the bank alone. None of them appear in any ICANN registry. None of them can be typosquatted, seized, or redirected. And each one carries a DANE-pinned TLS certificate that makes man-in-the-middle attacks cryptographically impossible.

When a customer logs in to accounts.bankname, the full trust chain works like this: the browser queries a Handshake-aware resolver, which verifies the .bankname TLD record directly against the blockchain. The DNSSEC chain is anchored at the HNS root — not at a CA. The TLS certificate is verified against the TLSA record, not against a list of 200 trusted authorities. The customer's identity is authenticated via a cryptographic signature, not a password transmitted over the network. No CA was trusted. No registrar was involved. No ICANN policy applied.

GDPR, KVKK, and Data Sovereignty

For banks operating in Turkey under KVKK or in the EU under GDPR, the data sovereignty implications are significant. Among financial service leaders surveyed for the 2026 API Security Impact Study, 96% reported at least one API security incident over the past 12 months — the highest among all industries. Many of those incidents originate at the DNS and certificate layer, not inside the bank's own systems.

Under ICANN DNS, DNS queries are logged by resolver operators — external parties the bank has no control over. Under Handshake, the bank runs its own resolver. No external telemetry. No third-party DNS logs. No registrar terms of service that limit what the bank can do with its own namespace.

GDPR Article 32 requires appropriate technical measures to ensure the security of processing. KVKK Article 12 requires equivalent technical safeguards. A Handshake TLD satisfies both more robustly than any ICANN-based configuration — not because of policy, but because the attack surface at the DNS layer is structurally eliminated.

What This Requires From a Bank

Adopting a Handshake TLD for banking infrastructure is a deliberate architectural decision, not a drop-in replacement. It requires:

- Acquiring the TLD via Handshake's on-chain Vickrey auction using Bob Wallet or the

hsdCLI - Running an authoritative nameserver (Bind9 or PowerDNS) on bank-controlled infrastructure

- Publishing DNSSEC DS records on-chain as the trust anchor

- Generating and publishing DANE TLSA records for all customer-facing services

- Deploying an HNS-aware recursive resolver (hnsd) within the bank's network

- Storing the TLD private key in a hardware security module with multi-sig governance

None of these steps are beyond the technical capability of a bank with a competent infrastructure team. The Handshake ecosystem has mature tooling — Bob Wallet, hnsd, the hsd full node — and growing documentation. The SkyInclude community and LearnHNS are the best starting points for teams exploring HNS integration for the first time.

The Bigger Picture

In 2023, financial institutions accounted for 27% of all breaches worldwide — surpassing even healthcare as the most breached industry. The attack surface keeps growing. Phishing, DNS hijacking, rogue certificates, registrar compromise — these are not exotic threats. They are the documented, recurring attack patterns that banking security teams fight every year.

Handshake TLDs do not solve every security problem a bank faces. But they close the DNS layer — permanently, cryptographically, and without dependence on any third party. For an industry where a single DNS hijack can redirect millions of customers to a phishing page while the SSL padlock stays green, that is not a minor improvement. It is a structural one.

The question is no longer whether decentralised DNS is technically viable — it demonstrably is. The question is which institution will be first to deploy it at the scale of a full banking namespace, establishing the security standard that others will follow.

Concept and architecture by Sina Khoshtarkib Zenoozi — Web3 · Blockchain DNS · FinTech Security, May 2026. For more on Handshake infrastructure, explore LearnHNS.